Topics The 38th Public Relations Seminar -ESG Management, Information Disclosure and Relationship with Society

The JPMA Public Affairs Committee held its 38th Public Relations Seminar on October 18, 2022, at Nomura Conference Plaza Nihonbashi (Chuo-ku, Tokyo). This year's seminar, titled "Relationship between ESG Management, Information Disclosure, and Society," featured Mr. Takayuki Sumida, Executive Officer of Sumitomo Corporation, who has extensive knowledge on the current trend of non-financial information disclosure and corporate integrated reporting.

Scene of the lecture

Scene of the lecture

In recent years, there has been a growing movement internationally to require companies to disclose non-financial information. In Japan as well, an increasing number of companies, both listed and non-listed, are becoming aware of the issue of disclosing non-financial information as part of their stakeholder communication. This is due to the fact that it has become increasingly difficult to determine corporate growth potential and market value based solely on financial information such as operating income in order to solve social issues such as global warming.

In this lecture, he explained how ESG*1 management and non-financial information have attracted attention in the transition from the 1980s to the present day, and gave specific Explanations on the trends of information disclosure, including integrated reporting, and the movement toward the establishment of rules for information disclosure that could become the standard in the future.

In addition, he emphasized the importance of creating a story of the company's corporate value, the necessity of clear intention of management, and the importance of "selecting" rules and standards according to the items that are important to each company, rather than exhaustively covering them.

In the Q&A session, PR committee members raised specific concerns about information disclosure directly related to their day-to-day work. In the post-conference questionnaire, participants responded, "I gained a great understanding of what I had studied in the book, as you explained it visually and with actual situations," and "I think my company's PR staff will be very pleased. I will give them feedback." These responses indicated that the seminar was practical for the participants.

Finally, Mr. Yasushi Okada, Chairman of the JPMA, commented, "I felt once again that the core of raising corporate value is to pursue and promote the company's social raison d'etre while paying close attention to the rules and standards and what is required of each company in the pharmaceutical industry. I felt again that the core of raising corporate value is to pursue the company's social significance while listening carefully to what is being demanded in terms of rules and standards.

The following is a recap of Mr. Sumida's speech.

-

1ESG: Acronym for Environment, Social, and Governance.

ESG management and information disclosure, and its relationship with society

Executive Officer of Sumitomo Corporation and President of Sumitomo Corporation Global Research, Inc.

Mr. Takayuki Sumida, Former Chairman of WICI (World Intellectual Capital/Assets Initiative)

Why is ESG management attracting attention?

What is the purpose of corporate management? Japan and other countries originally had different ways of thinking, but when the bubble economy burst in the 1990s, Japanese management lost confidence. The Japanese management changed drastically as the Western style of "take better care of shareholders" became the prevailing trend.

The 1990s was a time when the Cold War structure collapsed and the world became capitalist. In addition to the borders of people, the borders of money (capital) also disappeared, and the globalization of the world advanced rapidly. As a result, domestic companies have more and more foreign shareholders, and as a result, discussions are becoming more shareholder-centered in the short term, rather than just from a long-term perspective. Discussions will focus on revising Japanese accounting standards and that things like ROE*2 management should take place, and money-oriented, short-term management will become the norm.

In my opinion, this has caused a considerable blurring of the Japanese style of management. Originally, Japanese management was based on a long-lasting perspective that cherished nature, employees, family, and community, as in "sampo yoshi," or "good for the seller, good for the buyer, and good for the seller. It was not just about short-term money, but truly sustainable management that would last for more than 100 years based on "iye" (i.e., the family).

Japan has lost this Japanese style of management in the process of adapting to the rest of the world, but the world began to change around 2010, with the emergence of ESG and the Sustainable Development Goals (SDGs) around 2015. The Lehman Shock has changed the world in the short term. The collapse of Lehman Brothers has led to a demand for management not only from a short-term perspective, but also from the perspective of a broad range of stakeholders.

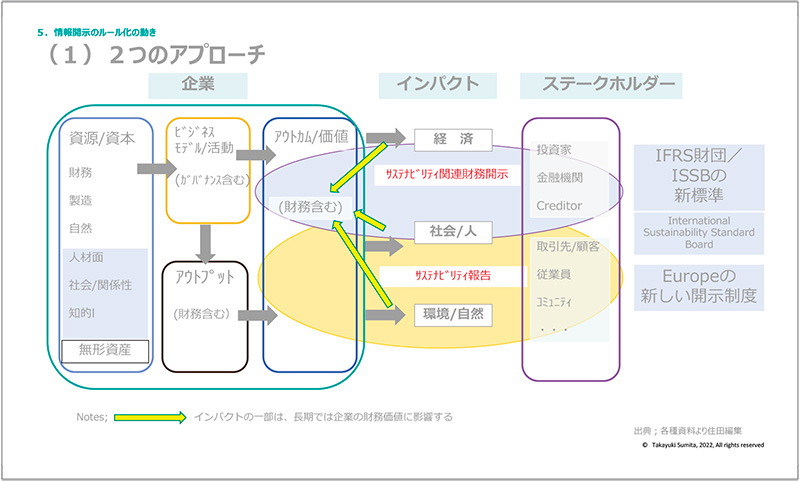

In this context, the important concept of Creating Shared Value (CSV) has emerged. The idea that creating this value is what management is all about is gaining ground. In addition, the emphasis is not only on outputs but also on the social impact of those outputs ( Figure 1 ).

-

2ROE (Return On Equity): Return on equity. A financial indicator that shows how much profit a company has generated from its own capital (shareholders' equity, etc.).

Figure 1 Capitalism itself is changing

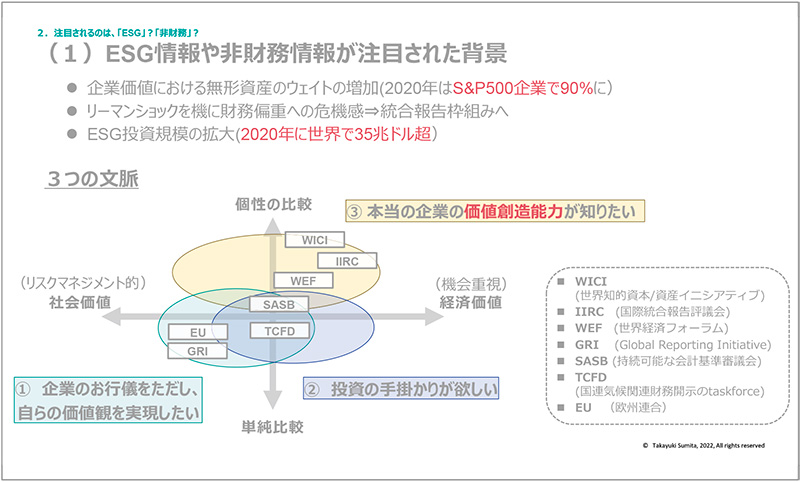

What should be focused on: "ESG" or "non-financial"? Non-financial factors?

There are three major contexts in which ESG information and non-financial information have attracted attention ( Figure 2 ).

(1) Skepticism about corporate behavior (to avoid corporate niceties and realize one's own values)

(2) Desire for investment clues

(3) Want to know the true value-creating ability of a company

Figure 2 Background of attention to ESG and non-financial information

(1) is more of a socialist concept. In European countries, there is skepticism about corporate behavior. Companies only pursue profits and are a burden to society. Therefore, they must be made to behave well." The European Commission of the EU is a typical example. You have to understand that the focus of ESG they focus on is negative check type items on various aspects such as environmental, social, human rights, corruption, and so on.

They make a list of "things a company should not do. Are we doing these items right?" What about this one? How about that one?" and then they list a lot of checkbox-type items. Western companies, even if they have a few items on the list, will say aggressively, "We are doing everything right here. However, serious Japanese people tend to take a flowery approach, saying, "We are doing this, we are doing that, we are doing everything," and Japanese companies are very weak in this check-box approach.

Next comes (2), the group that wants investment clues, the kind of people who have been selling funds by analyzing short-term numbers. Once financial engineering was developed, all kinds of analysis could be done on financial information, and the results would be the same no matter who did the analysis. They wanted another way to distinguish companies. They decided to focus on "non-financial information. The problem is that they want to "compare companies," so they demand that we answer all the questions for many easy comparisons.

Finally, group (3) is the group of people who thought that "if you really want to analyze a company, the non-financial part is important. The thought is that the value created by a company does not come from financial factors alone, and that the characteristics of a company are usually rooted in the non-financial part of the company, not the financial part. It is also the idea that what non-financial factors will be important will differ from company to company. A representative player of this (3) is the integrated reporting stream of the International Integrated Reporting Council (IIRC) and WICI*3, in which I have been involved for many years.

-

3WICI (The World Intellectual Capital/Assets Initiative): A partnership with private and public organizations to promote the development of intellectual assets/capital and key performance/value indicators (KPIs) that are of interest to shareholders and other stakeholders. Key Performance Indicator (KPI): An organization that partners with private and public organizations to improve disclosure of intellectual assets/capital and key performance indicators (KPI) of interest to shareholders and other stakeholders.

What is the relationship between corporate value creation and non-financial factors?

Let me tell you a little more about the relationship between corporate value creation and non-financials. The resources available to a company include "tangible assets," "intangible assets (intangibles)," and "external assets (assets of partners, etc.). While inputting these into the "value creation mechanism" of the company, or in other words, the business model, they are converted into value, which is the output. This is the value creation process of a company.

What kind of value does a company create? It will not only be economic value, but also social and environmental value. Also, "what kind of business model is used to achieve this" will be very unique, and the underlying "what kind of resources can be used" will differ from company to company. Intangibles such as intellectual assets that do not appear in financial information are the source of differentiation and rent (profit).

Therefore, good investors and analysts know that companies cannot be compared side by side. On the other hand, there are those who try to make simple comparisons, but companies should not be defeated by them. We must always recognize and insist, "We have this kind of individuality." This is important.

In the case of Japanese companies, "suriawase" in the manufacturing industry is a good example. This approach is a strength not found anywhere else in the world and is truly intangibles. Another strength of Japan is its relationship with its customers and the feedback it receives from consumers, its technological capability to produce high quality products, and its wide base of engineers.

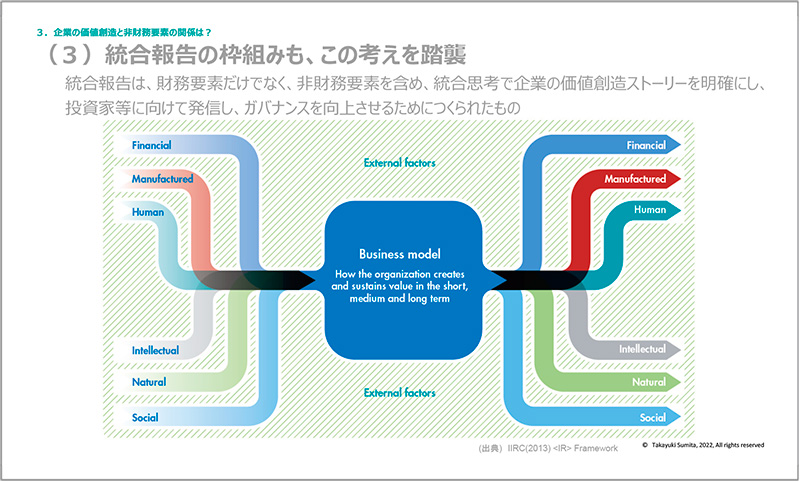

The framework for integrated reporting actually follows this kind of thinking. It seems to be foreign, but it is almost Japanese. There are six capitals on the input side, a business model in the middle, and various values that come out of the output side are returned to the original capitals. I think this is a very good mechanism.

This entire frame is called the business model, and governance is at the helm of the business model, and the higher-level concepts of purpose, mission, and vision, which express a sense of purpose and raison d'etre, are what integrated reporting conveys ( Figure 3 ). This is why we ask companies to "draw a value creation story" through the integrated report, and this is why it is important to create non-financial value rather than financial value.

Figure 3 Framework for integrated reporting

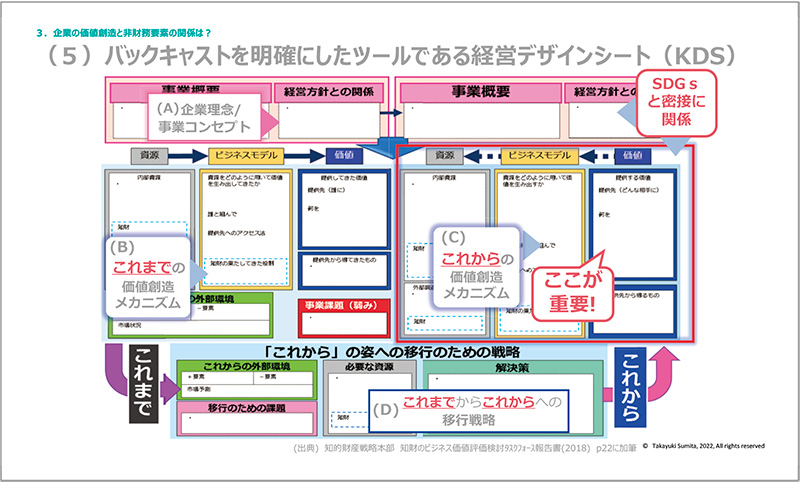

In 2018, we created the "Management Design Sheet" ( Figure 4) as a tool to help companies think about value creation. On the left side of this sheet (B), we write about the past: "What resources have we used, what business model have we used, and what value have we created so far? What is particularly important at this point is to think backward from the perspective of "what kind of value will we create" and "what kind of value do we want to create?

Figure 4 Management design sheet

The value that will be needed in the future world will change. When you want to create value, it will not be value unless it is shared by the world. For this reason, I think the most effective way now is to "translate it into the language of the SDGs. Once the image of value is clear, when you say, "This is what it means in terms of the SDGs," many people will sympathize with you and say, "Oh, I understand that! I understand that," and many people sympathize.

The arrows on the Management Design Sheet are reversed on the left and right, indicating that we are thinking in terms of backcasting here. Starting from the future, think about what to do by connecting the past with the future. Of course, the topmost Purpose and Corporate Philosophy (A) must be at the root of this thinking, but the strategy (D) must also be backcasted from the future value. This part is very important, which is indicated by the term "management design.

Trends in information disclosure, including integrated reporting

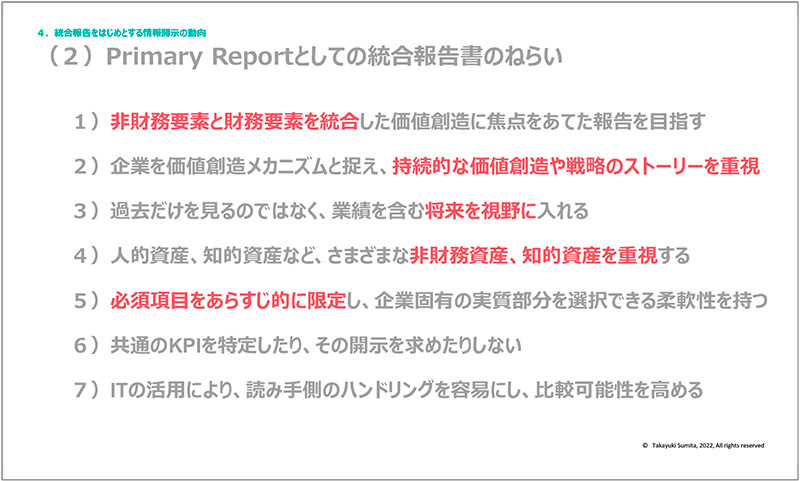

Integrated reporting is the primary report at the heart of the various reports issued by a company. The goal of integrated reporting is to "integrate financial and non-financial aspects" and to depict "value creation" and "strategic story" ( Figure 5 ). It does not specify key performance and value indicators (KPIs) or require disclosure of common KPIs. Recently, most integrated reports are about 100 pages long, but I think it is very important for the CEO to tell the essence of the story, even if it is shorter.

Figure 5 Aim of integrated reporting

The quality of integrated reports in Japan has become very high over the past three to four years, and WICI Japan holds an annual integrated reporting awards ceremony. The key points of the award-winning companies' integrated reports are that "financial and non-financial elements are integrated as integrated thinking," and that "the ability to create value over the medium to long term, which is corporate value itself, is clearly explained. The evaluation is not based on the variety of things written in the report, but on how persuasive this essential part of the report is.

On the other hand, integrated reports that are increasingly subdivided by business unit are often unclear: the CEO's message is very abstract, and then it is very difficult to understand the sudden leap to talking about finance and each business unit. Also, everyone draws a picture of the value creation mechanism, but there are few explanations. I think it would be easier to understand if the precise explanation is written as a story where there is a picture.

Trends in disclosure rules

The first is standardization following the IIRC's integrated reporting approach . The first is standardization following the IIRC's concept of integrated reporting. The International Sustainability Standards Board (ISSB) standard is being developed based on the concept of "reporting on what investors consider important in terms of corporate value.

In contrast, the second approach of the European Commission is different. Europe is interested in corporate behavior, so the new disclosure system is based on the idea that "if a company's activities have an impact on society, the economy, or the environment, it should be reported. In other words, it will be a check-the-box type system in which all items that have more than a certain degree of impact are to be reported, even if they do not relate to corporate value.

Figure 6 Two approaches

The ISSB has issued a draft standard for 2022. There are "general requirements" and "thematic requirements," and one of the thematic requirements is climate-related. The four elements to be disclosed are "governance," "strategy," "risk management," and "measurement methods and targets," and are a compilation of what various organizations have been working on. On the other hand, Europe is in the process of creating various rules and trying to apply them in a sort of extraterritorial way, and it seems that if there is a subsidiary of a certain size in Europe, the parent company will be required to disclose as well. If this is realized, the impact is likely to be very large.

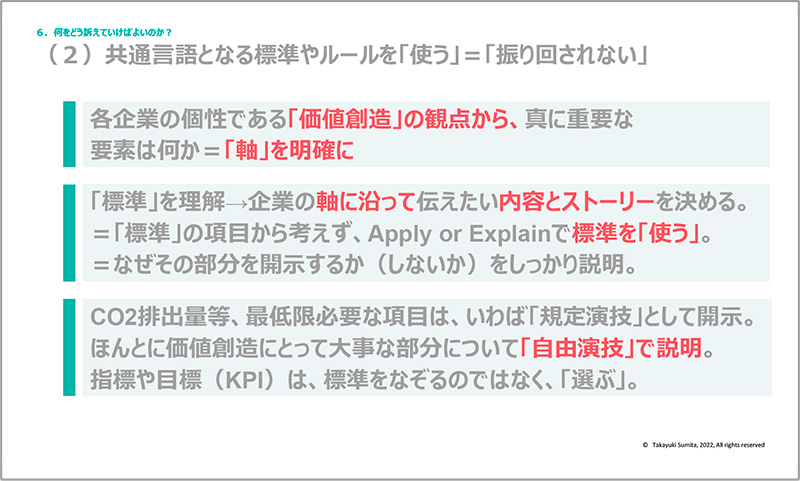

What should we appeal?

First of all, we need to clarify "what we want to do as a company" and "why we are doing it" as the axis of our business. Then, we will communicate "what kind of value (positive or negative) we are actually creating," "what kind of business model we have, what kind of strategy, what kind of resources we are using," and "who we are doing it for and for what purpose.

This is both to communicate to stakeholders and for internal consistency. It does not matter what medium is used for disclosure, but it is important to have a "coherent axis. Japanese people tend to focus on strict adherence to rules and standards. In particular, when management tells the IR or sustainability department to "make it right," without giving firm instructions, the department will definitely go into a "defensive" stance that covers the rules and standards. This will result in a report that has "no intention," "very little value," and is "unusually labor-intensive.

Rules should be used, not swept under the rug ( Fig. 7 ). In particular, a standard is a kind of dictionary. Therefore, each company should indicate the items that they think are important by using the definitions or calculation methods in the standards. It is not necessary to cover all the items in the standard at all. A standard is "apply or explain. It is sufficient to explain that this item is important, so the standard is applied, while this item is not important, so it is not written. If we think in such an approach, we can create a very reasonable integrated report, which I believe will be the integrated report that true investors and stakeholders really need.

Figure 7 What should we emphasize?

( Takafumi Adachi, General Manager, Public Relations Department)